If you’ve been searching for quick cash online and stumbled across eLoanWarehouse, you’re not alone. Thousands of Americans type “payday loans eLoanWarehouse” into search engines every month, hoping to find a fast financial lifeline. But before you fill out that application, there are some important facts you need to understand — facts that most other articles don’t fully cover.

This guide gives you a complete, honest, and up-to-date picture of what Payday Loans eLoanWarehouse actually is, how it works, what it costs, and what your Payday Loans eLoanWarehouse are.

What Is eLoanWarehouse?

eLoanWarehouse is an online short-term lender headquartered in Hayward, Wisconsin. It is operated by LCO Financial Services, a business entity of the Lac Courte Oreilles Band of Lake Superior Chippewa Indians — a federally recognized Native American tribe.

The company offers installment loans ranging from $300 to $3,000 and markets them as a more affordable alternative to traditional payday loans. Unlike a single lump-sum payday loan that must be repaid in full on your next paycheck, eLoanWarehouse lets you repay in scheduled installments over time. They also have a dedicated mobile app available on both iOS and Android.

At a glance, this sounds reasonable. But once you look at the actual numbers, the full picture becomes a lot more complicated.

Is eLoanWarehouse a Payday Loan Company?

This is where many borrowers get confused. eLoanWarehouse technically calls its products installment loans, not payday loans. The key difference is repayment structure:

- A payday loan is typically due in full on your next payday (2–4 weeks).

- An installment loan is repaid over multiple scheduled payments — which can span several months.

However, the interest rates and overall cost structure at eLoanWarehouse are very similar to those of traditional payday lenders, which is why the two terms are often used interchangeably when people search for this company online.

What Does eLoanWarehouse Actually Cost?

This is the section most other articles gloss over. Let’s be direct.

Interest Rates (APR)

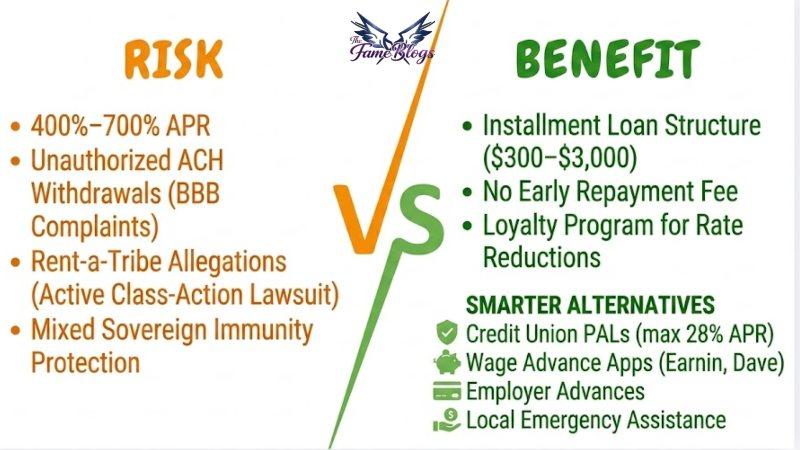

eLoanWarehouse does not prominently advertise a specific APR on its homepage, but borrowers and financial review platforms consistently report APRs ranging from 400% to 700%. To put that in perspective, the average personal loan from a bank carries an APR of 10%–36%.

One documented borrower complaint describes taking an $800 loan that ended up requiring over $2,676 in total repayments. That’s more than three times the original loan amount.

Fees You Should Know About

- Upfront/origination fee: Charged at the time of the loan

- Finance charges: Interest that accrues over your repayment period

- Late payment fee: Applied if you miss a scheduled payment

- Rollover or extension fee: If you need more time to pay, additional fees apply

One important note that works in eLoanWarehouse’s favor: they do not charge an early repayment fee. If you can pay off your loan ahead of schedule, you won’t be penalized — and you’ll save significantly on interest. This is worth taking advantage of if you do take out a loan.

While the company doesn’t list specific rates on their homepage, independent financial reviews of eLoanWarehouse and borrower reports consistently show APRs ranging from 400% to 700%.

The Loyalty Program

eLoanWarehouse operates a tiered loyalty program. When you make consistent, on-time payments, you can advance through program tiers that may qualify you for better rates on future loans. This is something most competitors don’t offer and is worth knowing about — but it only benefits borrowers who can manage their payments reliably.

Tiered incentives and loyalty rewards are common strategies used by modern digital platforms to keep users coming back. You can see similar engagement tactics used in our analysis of Trendywinner.com’s user experience, where we discuss how sites align with current internet trends to build an active audience.

The Tribal Lender Factor: What It Means for You

Here’s something you’ll rarely find explained clearly in other eLoanWarehouse articles: the tribal lender legal structure and why it matters for borrowers.

Because eLoanWarehouse is operated by a tribal entity, it claims protection under tribal sovereign immunity — meaning it may not be subject to the same state-level interest rate caps and consumer protection laws that apply to regular lenders in your state.

For example:

- Virginia generally caps loan interest at 12% per year

- North Carolina caps it at 8% per year

- Illinois has strict payday loan rate caps

In states like these, a regular lender could not legally charge 400%+ APR. But a tribal lender may argue those state caps don’t apply to them.

However — and this is important — this legal shield is not airtight. Federal consumer protection laws, including the Truth in Lending Act (TILA), still apply to tribal lenders regardless of sovereign immunity. TILA requires clear disclosure of APR, finance charges, and total repayment amounts before you sign.

Courts have also rendered mixed decisions on whether tribal immunity fully protects these lenders. Some rulings have found that immunity does not apply when the tribe is not the true controller of the lending operation.

Navigating the complexities of digital business ethics requires a deep understanding of who is really behind the curtain. For a look at how true influence is wielded in the technology sector, read our profile on Silicon Insider Gordon James, which explores the real story behind a quiet but significant tech power.

The Class-Action Lawsuit Against eLoanWarehouse

This is a critical piece of information that most articles either miss entirely or mention only briefly.

A class-action lawsuit was filed alleging that the companies behind eLoanWarehouse.com are engaged in an illegal “rent-a-tribe” scheme — a practice where a non-tribal payday lender claims its business is owned and operated by a Native American tribe specifically to bypass state interest rate caps.

The lawsuit, which names Opichi Funds LLC as a defendant, claims that while the Lac Courte Oreilles Band is listed as the lender, non-tribal entities actually control the lending operations — including marketing, underwriting, and collections — from locations far from tribal land and performed largely by non-tribal members. The suit alleges this arrangement violates state usury laws.

The case looks to represent Illinois residents who received loans at more than 9% interest that have not been paid in full.

This lawsuit does not mean eLoanWarehouse is a scam. The company does fund loans and has an A+ BBB rating. But it does mean there are unresolved legal questions about whether the loans it offers are enforceable under your state’s law. If you’re in a state with strict rate caps and you take a loan from eLoanWarehouse, it’s worth being aware that courts in some states have found similar loans unenforceable.

BBB Complaints: What Real Borrowers Are Saying

eLoanWarehouse holds an A+ rating with the Better Business Bureau, but that rating reflects responsiveness, not necessarily borrower satisfaction. Looking at the actual complaint history reveals some specific patterns worth knowing:

- Multiple borrowers report unauthorized ACH withdrawals from their bank accounts — amounts pulled on incorrect dates or for amounts not agreed upon in the loan contract

- One borrower reported that after a system update, the company repeatedly debited funds without authorization — five times in three weeks — causing overdrafts and significant stress

- Some borrowers report that after settling an account for a specific amount, the agreed-upon deduction was not processed, then they were threatened with full balance collection including late fees

- At least one borrower reported that eLoanWarehouse pulled a credit inquiry without clear authorization

If you do borrow from eLoanWarehouse, financial experts recommend monitoring your bank account closely for at least the full duration of the loan repayment period.

Who Qualifies for an eLoanWarehouse Loan?

The eligibility requirements are less strict than traditional lenders, which is part of why the company appeals to people who’ve been turned down elsewhere:

- At least 18 years old (some states require 21)

- U.S. citizen or legal permanent resident

- Minimum monthly income of $1,000 from employment, self-employment, Social Security, or disability

- An active checking account in your name

- Valid government-issued photo ID

- A U.S. residential address and working phone or email

eLoanWarehouse does not require a minimum credit score. They perform a soft credit check during the application, which does not affect your credit score. However, if you later request a larger loan, a hard inquiry may be triggered — so monitor your credit reports.

How the Application Process Works

- Visit eloanwarehouse.com and click “Apply Now”

- Enter personal details: name, date of birth, Social Security number, contact info

- Provide income information: employer, pay amount, next expected paycheck date

- Submit your checking account routing and account number

- Select your loan amount and review the fee schedule shown on screen

- Authorize the soft credit check

- Review all disclosures and submit

If approved, funds are typically deposited within one business day. Some borrowers report receiving funds within hours via direct deposit.

Important: Always select direct deposit rather than a prepaid card option if offered. Prepaid cards can carry hidden activation or monthly fees that are not included in the loan’s disclosed fee table.

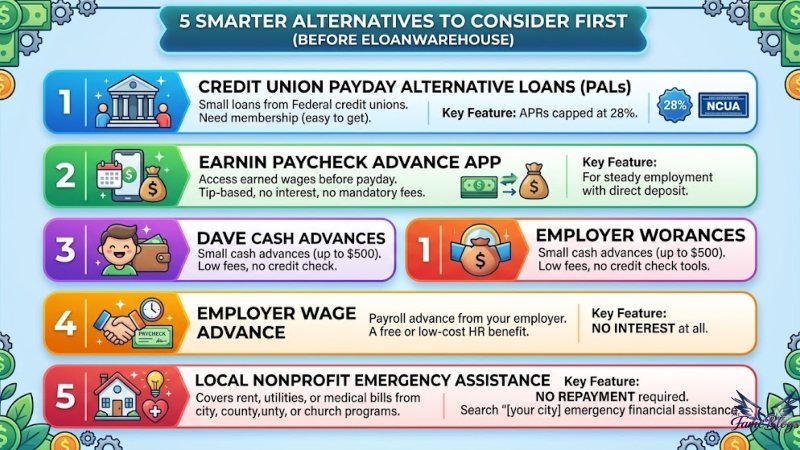

5 Payday Loans eLoanWarehouse to Consider First

Before applying to eLoanWarehouse, here are alternatives that may cost you significantly less:

1. Credit Union Payday Alternative Loans (PALs)

Federal credit unions offer PALs — small loans of $200 to $1,000 with APRs capped at 28% by the National Credit Union Administration. You need to be a member, but membership is often easier to obtain than people assume.

2. Earnin

A paycheck advance app that lets you access earned wages before payday. Works on a tip-based model with no mandatory fees and no interest. Best for people with steady employment and direct deposit.

3. Dave

Offers small cash advances (typically up to $500) with transparent, low fees and no credit check. Also includes budgeting tools to help prevent repeat borrowing.

4. Employer Wage Advance

Many employers offer payroll advances as a free or low-cost HR benefit. Ask your HR department — the answer may surprise you, and there’s no interest at all.

5. Local Nonprofit Emergency Assistance

Many cities and counties have nonprofit, church-based, or government emergency assistance programs that cover rent, utilities, or medical bills with no repayment required. Search “[your city] emergency financial assistance” to find programs near you.

Choosing a lower-cost alternative isn’t just about saving money—it’s about protecting the resources you need to enjoy your passions, much like how the CaliDancingFool lifestyle prioritizes community and movement over stress.

A Realistic Cost Comparison

| Option | Typical APR | Loan Amount | Credit Check |

| eLoanWarehouse | 400%–700% | $300–$3,000 | Soft check |

| Credit Union PAL | Up to 28% | $200–$1,000 | Yes |

| Earnin | 0% (tips optional) | Up to earned wages | No |

| Dave | Low flat fee | Up to $500 | No |

| Personal bank loan | 10%–36% | $1,000+ | Yes |

| Credit card cash advance | 25%–30% | Varies | No new check |

When eLoanWarehouse Might Make Sense

Despite the high costs, there are narrow circumstances where eLoanWarehouse may be a rational short-term choice:

- You face a genuine, one-time emergency (car repair, medical bill) that cannot wait

- You have no access to cheaper alternatives — no credit union membership, no credit card, no employer advance

- You can realistically repay the full amount (principal + all fees) within your repayment schedule — without needing to roll it over

- You understand the full cost going in and have budgeted for repayment

If you can’t say yes to all four of those conditions, the math will likely work against you.

5 Signs You Should Skip eLoanWarehouse

- You cannot repay the full amount by your scheduled due dates

- You’ve already taken a payday or installment loan in the past 90 days

- You’re borrowing to cover essential expenses like rent, groceries, or utilities

- The disclosed APR is substantially higher than you expected

- A credit union loan, personal loan, or advance app is available to you

Protecting Yourself If You Do Borrow

If you decide to proceed with eLoanWarehouse after weighing everything, take these steps:

- Screenshot every screen of the loan agreement before signing

- Set up account alerts on your bank for all transactions

- Do not give authorization for amounts or dates beyond what’s in your signed agreement

- Know your right of rescission — in most cases, you can cancel the loan within three business days of signing without penalty

- If the company makes unauthorized withdrawals, file a complaint immediately with the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov/complaint and with your state attorney general

Final Verdict

eLoanWarehouse is a legitimate, licensed lender that does fund loans quickly and serves borrowers who have been turned down elsewhere. The no-early-payoff-fee policy and loyalty program are genuine positives. But the triple-digit APRs, documented unauthorized ACH complaints, and an active class-action lawsuit involving rent-a-tribe allegations mean this is not a lender you should turn to without doing your homework first.

For most Americans facing a short-term cash crunch, a credit union PAL, a paycheck advance app, or an employer wage advance will cost dramatically less and come with fewer legal complications.

If eLoanWarehouse is your only option, go in with your eyes open, borrow the minimum amount you actually need, and pay it off as fast as humanly possible.

Disclaimer: This article is for informational purposes only. TheFameBlogs.com is not a financial advisor. Always consult a licensed financial professional before making borrowing decisions.